When dealing with a company valuation with excess cash, what steps to take first? First, you need to make a split. Apple valuation is a very good sample and it can be done in a simple manner.

I split Apple into Cash Apple and Operating Apple as follows. Assuming required normalized operating cash is the exercise to be done.

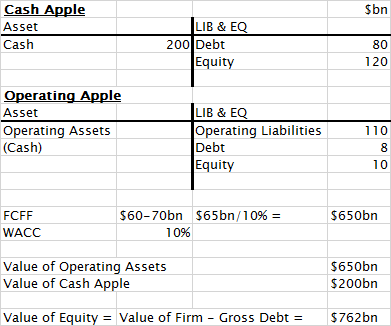

Cash Apple

Asset

Cash $200bn

Liabilities & Equity

Debt $80bn

Equity $120bn

Operating Apple

Asset

Operating Assets $127bn (including $38bn cash)

Liabilities & Equity

Operating Liabilities $110

Debt $7bn

Equity $10bn

D/E ratio is assumed to be the same for each.

Other key valuation assumptions:

FCFF is around 60-70bn, and use the middle $65bn for valuation.

FCFF is to estimated to grow low single-digit.

WACC is 10% in my spreadsheet.

In case FCFF growth is zero, the value of equity is $65/10% + ($200bn-$80bn) = $770bn($146).

If FCFF growth is 2%, ges $65/10% to $65/8% so that the sum will go to $932bn.

Likewise, if growth is -2% growth, changes the sum to $660bn ($125).

Very conservatively assuming -4% growth equals to $584bn ($111), close to the market price recently.

Future growth trajectory does matter a lot, but investing at around $110 of the current market price level seems substantially reasonable and very conservative.

Perhaps the so-called market consensus (in fact it is the average of 6-9 months horizon price forecast) would move around $170-200. But that is not what long-term investors should focus on.

How Apple’s excess cash will be spent or utilized is sure to change the way Apple is valued.

Regardless, Apple is even better positioned than before. Many are missing the point that Apple is establishing itself as a platform-based consumer technology company. It is the next-gen Apple, which graduated from the narrowly focused & device reliant business model. The key differentiation is the user-oriented culture and customer-focused policy. Users and paying customers are matched for Apple, making it consistent and robust to focus on the real value it has to deliver.

That is not always the case for consumer tech companies, however. Especially the consumer-focused technology service companies born from the internet tend to have bipolar markets, and the people who pay are not the people who receive its service, implying a structural conflict that may become apparent sometime in the future.